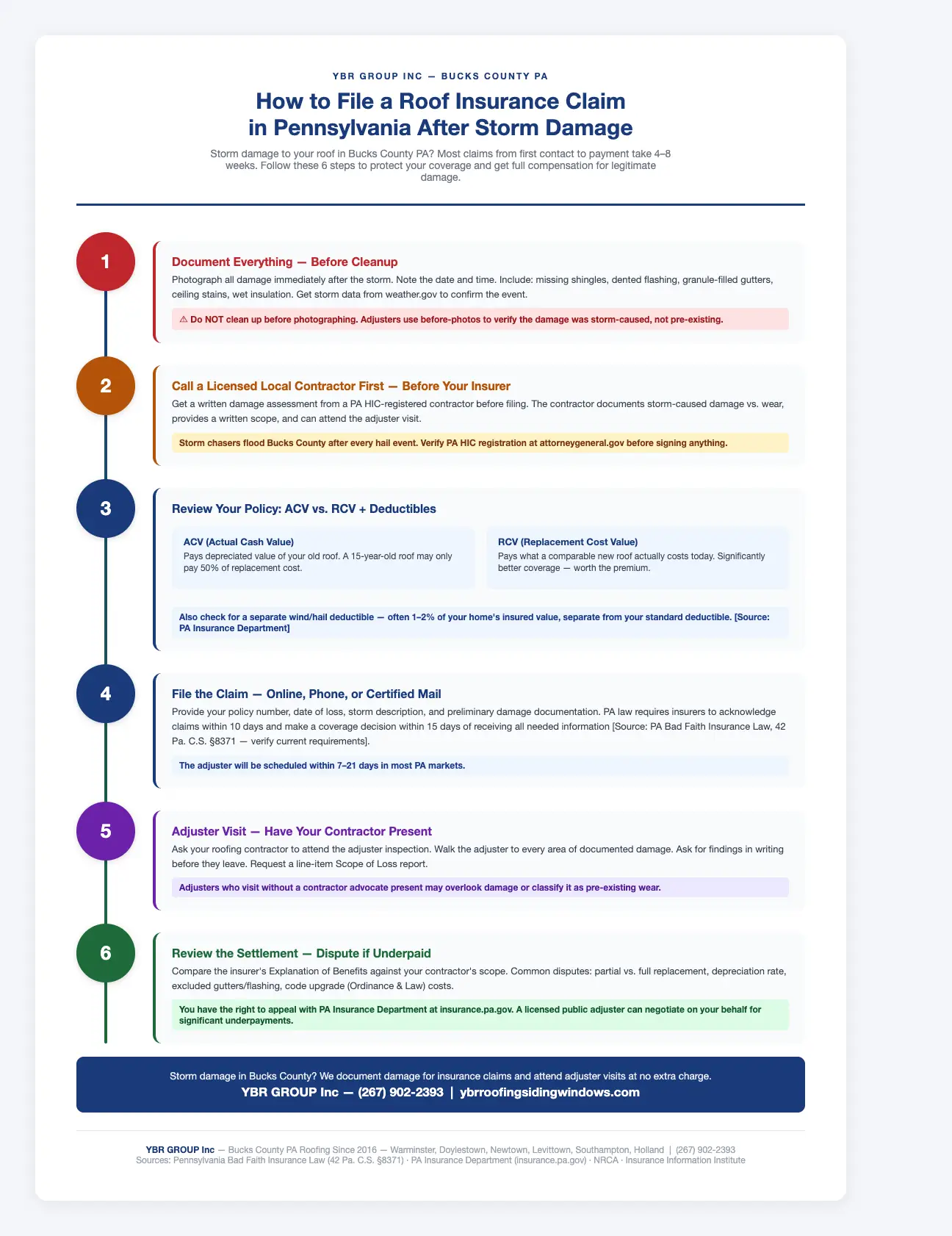

Roof Insurance Claim Pennsylvania: Step-by-Step Guide After Storm Damage

A hailstorm rolls through Warminster. A nor’easter tears shingles off rooftops in Levittown. Wind-driven rain soaks attic insulation in Doylestown. When storm damage hits your roof in Pennsylvania, the insurance claim process can feel overwhelming — especially if you’ve never filed one before. This guide walks Bucks County homeowners through every step, from documenting damage to getting your roof replaced without out-of-pocket surprises.

Step 1: Document Roof Storm Damage Immediately

The moment it’s safe to do so after a storm, document all visible damage. Your insurance company will require evidence, and the more thorough your documentation, the stronger your claim.

- Photograph your roof from the ground at multiple angles

- Document all damaged areas: missing shingles, dented flashing, cracked ridge caps, gutters full of granules

- Photograph interior damage too — ceiling stains, wet insulation, damaged drywall

- Note the date and time of the storm event

- Collect any storm data records (weather.gov reports, newspaper coverage of the storm event)

Do not attempt to walk on your roof after a storm — contact a licensed roofing contractor for a professional inspection instead.

Step 2: Contact a Licensed Pennsylvania Roofing Contractor First

Before you call your insurance company, get a professional roof inspection from a licensed contractor. This is especially important in Bucks County PA where storm chasers and out-of-state contractors often descend after major weather events.

A qualified local contractor will:

- Document all damage with photos and written notes

- Identify storm-caused damage vs. pre-existing wear (a critical distinction for your adjuster)

- Provide a written damage assessment and preliminary scope of work

- Be available to meet your insurance adjuster on-site

YBR GROUP Inc has been handling storm damage assessments for Bucks County homeowners since 2016. Our team documents damage thoroughly to support homeowners through the claims process — we understand what Pennsylvania adjusters look for.

Step 3: Review Your Pennsylvania Homeowner’s Insurance Policy

Before filing, understand your coverage. Pennsylvania homeowner’s policies vary significantly between carriers and policy generations. Key items to review:

- ACV vs. RCV: Actual Cash Value (ACV) policies pay the depreciated value of your old roof. Replacement Cost Value (RCV) policies pay what it actually costs to replace it. Know which you have.

- Deductible: Most Pennsylvania policies have a standard deductible ($500–$2,500 is common) AND a separate wind/hail deductible — often calculated as a percentage (1–2%) of your home’s insured value [ESTIMATED — verify with your policy documents].

- Covered perils: Confirm that hail, wind, and the specific type of storm are covered events.

- Exclusions: Pennsylvania policies typically exclude damage from “neglect,” “wear and tear,” and “faulty installation.” An insurer may attempt to reclassify storm damage as maintenance neglect.

- Claim filing window: Most Pennsylvania policies require claims to be filed within a reasonable time after the loss. Check your policy’s specific language.

Step 4: File the Roof Insurance Claim in Pennsylvania

Once you have your contractor’s damage assessment, contact your insurance company to open a claim. You can typically file:

- Online through your carrier’s claims portal

- By phone to your insurance agent

- Via a written letter (send certified mail for documentation)

Provide: your policy number, date of loss, description of the storm event, and your preliminary damage documentation. The carrier will assign a claim number and schedule an adjuster visit — typically within 7–21 days in Pennsylvania [Source: Pennsylvania Insurance Department consumer guidance; verify with your carrier].

Step 5: The Insurance Adjuster Visit — What to Expect in Bucks County

Your insurer will send an adjuster to inspect the damage. This inspection determines what the insurance company will pay. Key strategies for Bucks County homeowners:

- Have your contractor present: Ask YBR GROUP (or your chosen contractor) to attend the adjuster visit. A contractor advocate on-site ensures the adjuster doesn’t overlook damage.

- Walk the adjuster to every area of damage — don’t assume they’ll find everything independently.

- Ask for the adjuster’s findings in writing before they leave the property.

- Request line-item detail in the Scope of Loss report the adjuster produces.

Step 6: Review the Insurance Estimate and Negotiate if Necessary

After the adjuster visit, your insurance company will issue an Explanation of Benefits (EOB) or claim settlement estimate. Compare it carefully against your contractor’s assessment. Common disputes include:

- Adjuster estimating partial replacement; contractor documenting full replacement is required

- Depreciation applied at a higher rate than justified by roof age

- Code upgrade costs excluded (Pennsylvania code compliance upgrades are often a covered add-on called “Ordinance or Law” coverage)

- Gutters, flashing, or skylights excluded despite documented storm damage

You have the right to dispute the settlement. Pennsylvania Insurance Department (PID) provides a formal appeals process. If a significant gap exists, a licensed public adjuster can negotiate on your behalf [Source: Pennsylvania Insurance Department, pa.gov/agencies/insurance].

EEAT: YBR GROUP’s Storm Damage Experience in Bucks County

Since 2016, YBR GROUP Inc has helped dozens of Bucks County homeowners navigate storm damage claims — from hail events across Warminster and Southampton to wind damage throughout Holland and Lower Makefield. We understand the difference between storm-caused damage and normal aging, and we document accordingly. We work alongside your adjuster — not against the process — to ensure legitimate damage is fully captured in the claim scope.

What If My Roof Insurance Claim Is Denied in Pennsylvania?

Claim denials happen. Common reasons include: insufficient documentation, the insurer classifying damage as wear-and-tear, or policy exclusions. Your options in Pennsylvania:

- Request a written explanation of the denial (required by PA law)

- File an appeal with your insurer’s internal review process

- Engage a licensed public adjuster to re-document the loss

- File a complaint with the Pennsylvania Insurance Department at insurance.pa.gov

- Consult a Pennsylvania policyholder attorney for bad faith claim handling

Frequently Asked Questions: Roof Insurance Claims in Pennsylvania

How long does a roof insurance claim take in Pennsylvania?

Pennsylvania insurance law requires insurers to acknowledge claims within 10 days and make a coverage decision within 15 days of receiving all necessary information [Source: Pennsylvania Bad Faith Insurance Law, 42 Pa. C.S. § 8371; verify current requirements with an insurance professional]. In practice, most roof claims from first contact to payment take 4–8 weeks depending on adjuster availability and any dispute resolution.

Will my homeowner’s insurance rates go up if I file a roof claim in PA?

Filing a claim may affect your premium at renewal, depending on your insurer and your claims history. However, most Pennsylvania carriers treat weather-related claims differently from liability or at-fault claims. Consult your agent before filing if you’re concerned about premium impact on borderline damage situations.

Can my contractor negotiate my insurance claim in Pennsylvania?

Your roofing contractor can document damage, provide a repair/replacement scope, and be present during the adjuster inspection to point out damage. However, contractors are not licensed to negotiate insurance settlements on your behalf — that role belongs to licensed public adjusters. YBR GROUP can support your claim with thorough documentation and adjuster coordination.

What is the difference between ACV and RCV on a Pennsylvania roof claim?

ACV (Actual Cash Value) pays the depreciated value of your old roof — meaning if your 15-year-old roof had 50% remaining useful life, you’d receive approximately 50% of replacement cost. RCV (Replacement Cost Value) covers what it actually costs to replace the roof with comparable materials today. RCV policies typically cost more in premium but provide significantly better coverage after a storm loss.

Ready for a free estimate? Call YBR GROUP Inc at (267) 902-2393 or contact us today. We serve Warminster, Levittown, Doylestown, Newtown, Southampton, Holland, Lower Makefield, and all of Bucks County PA.